Key takeaways

It now takes the median-income household over 8 years to save for a 20% deposit, compared to just 6 years in the early 2000s.

This “deposit gap” has become the single biggest hurdle for first-home buyers.

A typical new home loan consumes around 54% of household disposable income—the highest level in at least 20 years.

Home ownership rates for Australians under 34 have dropped sharply across every state, particularly in NSW and Victoria.

Those born in the late 1980s and early 1990s are significantly less likely to own a home compared to Baby Boomers, highlighting a structural intergenerational inequality.

The decline in young home ownership is not unique to Australia—it’s also seen in the UK, US, and Europe.

Contributing factors include insecure work, later marriage, and fewer children, which reduce the urgency or ability to buy a home.

Remember when owning a home was considered a rite of passage? A marker of stability and success?

Today, for many Australians, that milestone feels more like a distant fantasy than a realistic goal.

What was once seen as the cornerstone of financial security has become an uphill battle, with soaring property prices, stricter lending rules, and wages that simply haven’t kept pace.

Owning a home has always been the cornerstone of the Australian dream.

But for younger generations, that dream is slipping further out of reach.

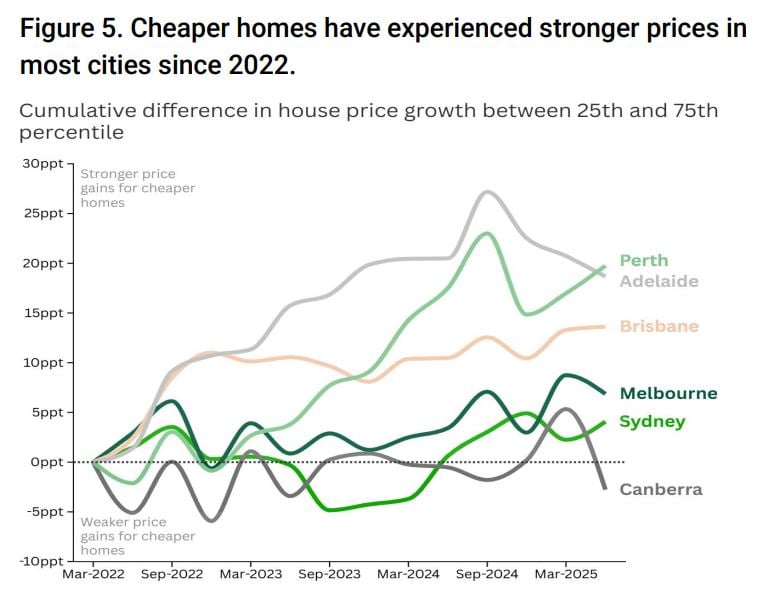

“Affordable” homes are becoming unaffordable

According to research by Domain, houses priced in the 25th percentile – typically purchased by first home buyers – have increased in price at a greater rate than premium houses (those in the 75th percentile) across most major capitals since 2022 – as the figures below show.

Cumulative difference in house price growth for entry-level homes compared with premium homes:

- Sydney: 4.1 ppts

- Melbourne: 6.9 ppts

- Brisbane: 13.6 ppts

- Adelaide: 18.7 ppts

- Perth: 19.8 ppts

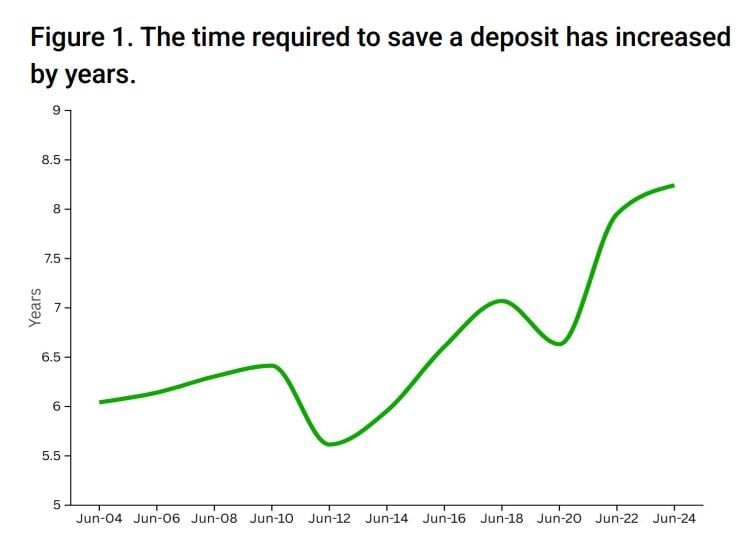

The deposit mountain

The biggest barrier for first-home buyers isn’t servicing the loan—it’s scraping together the deposit.

According to Domain, a median-income household now needs more than eight years to save for a 20% deposit, compared to just six years in the early 2000s.

Source: Domain

Dr Nicola Powell, Domain’s Chief of Research and Economics, says this has reshaped the entry point into the market:

“The time it takes to save a deposit has blown out dramatically.

For many first-home buyers, it’s not the repayments that keep them out of the market, it’s the sheer challenge of getting a foothold with such a large upfront cost.”

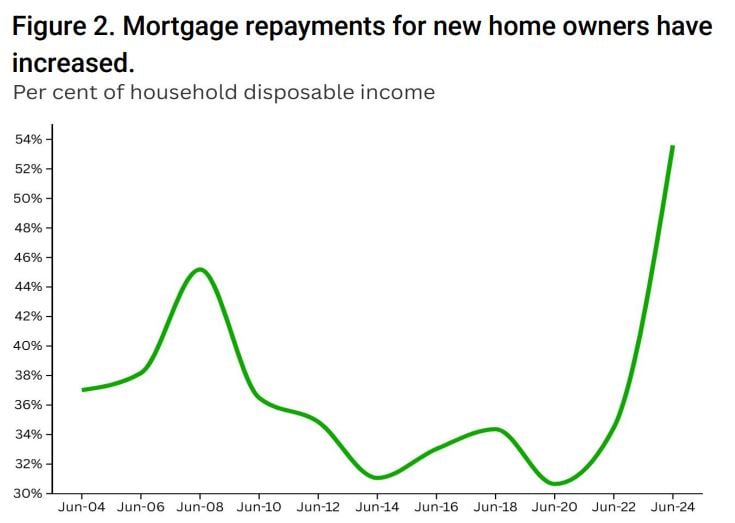

Mortgage stress at record highs

Even once buyers leap the deposit hurdle, they face much tougher repayments.

A typical new loan now consumes around 54% of disposable household income, the highest level in more than 20 years.

Source: Domain

This shift has been driven by the double blow of rapidly rising property prices and the sharp lift in interest rates after 2022.

While rate cuts in 2025 offered some relief, prices kept surging, offsetting much of the benefit.

Dr Powell notes:

“We’ve moved into a world where home ownership is becoming more exclusive.

Lower interest rates in recent years did help with repayments, but because prices rose even faster, the affordability equation actually worsened for many.”

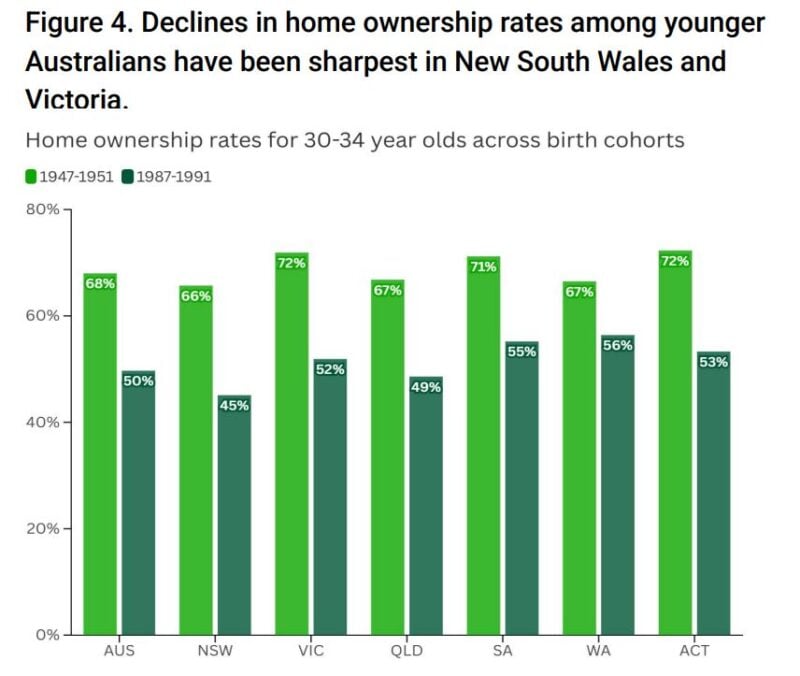

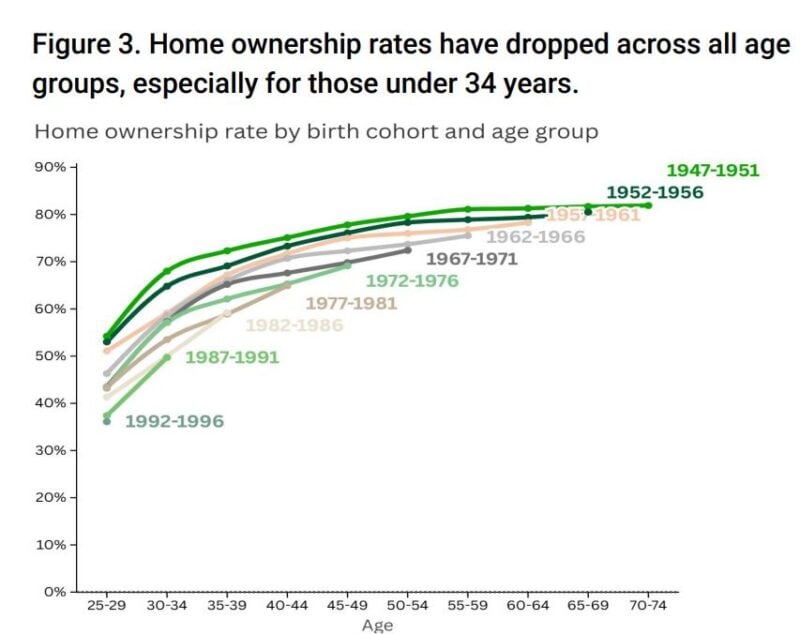

A widening generational divide

The impact is starkest among younger Australians.

Home ownership rates for under-34s have dropped across every state, with the sharpest falls in New South Wales and Victoria.

Source: Domain

The data shows that those born in the late 1980s and early 1990s are far less likely to own a home than those born just a generation earlier.

In contrast, many Baby Boomers benefited from decades of rising values, cheaper credit, and lower deposit hurdles.

Source: Domain

As Dr. Powell puts it:

“The generational divide in home ownership is the widest we’ve seen in modern history.

Younger Australians are being locked out, while existing owners see their wealth grow.”

A global trend with local consequences

This isn’t just an Australian story.

Studies show similar declines in home ownership among younger households across the UK, US, and Europe.

Contributing factors include later marriage, fewer children, greater income volatility, and the rise of insecure work.

Here in Australia, affordability pressures are also changing buyer behaviour.

Lower-priced homes have outperformed premium properties in price growth since 2022, particularly in Perth, Brisbane, and Adelaide.

Source: Domain

Search trends reveal more Australians now looking for “dual”, “granny” and “duplex” properties, reflecting rising interest in higher-density and more affordable housing options.

What needs to change?

The affordability challenge is structural, not cyclical.

It’s not just about where interest rates sit today.

Barriers like stamp duty, restrictive lending standards, and surging deposit requirements are locking more people out each year.

Potential reforms flagged by Domain include:

-

Replacing stamp duty with a broad-based land tax, to reduce upfront costs and improve mobility.

-

Expanding shared-equity and low-deposit schemes, to bridge the deposit gap for first-home buyers.

-

Reviewing lending standards, to strike the right balance between stability and access to credit.

Dr Powell concludes:

“If we want to restore the Australian dream of home ownership, we need coordinated reform.

Without it, the divide between the housing haves and have-nots will only deepen.”

Final thoughts

The numbers are clear: affordability has reached breaking point.

For first-home buyers, the challenge isn’t just paying off a mortgage, it’s finding a way to even get in the game.

And unless structural reforms are made, home ownership risks becoming a privilege for the few, rather than the foundation of financial security it has long been in Australia.